Shakespeare Blog: View from the Lake

A Year in Review: Economic Updates from 2023

Written By: Nick Ziarek, CFA, CFP®

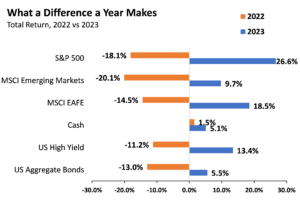

It may be cliché, but what a difference a year makes! Following a rocky 2022, which saw the worst year ever for the bond market and the seventh worst year for the stock market, 2023’s outlook was bleak.

Inflation was still high, the Federal Reserve was signaling more interest rate increases to come, and concern was growing that a soft landing for the economy was not in the cards. Add on a regional banking crisis with the bankruptcy of Silicon Valley Bank, Signature Bank, and First Republic Bank (three of the four largest bank failures in US history) and sprinkle in a dose of the drama and theater of the political showdown around the US debt ceiling and government shutdown and you had a recipe for another rocky year.

Despite those headwinds, by early June the S&P 500 had rallied more than 20% from October 2022 lows and officially entered a new bull market. The exuberance would continue as the Fed paused for the first time in June, more than a year after the start of the most aggressive rate hiking cycle in decades. At that time inflation had declined to 2.97% (from its peak of 9.1% in June 2022) and the unemployment rate remained near historic lows while the economy continued to show modest growth. Anticipation built when the Fed pulled off the impossible, avoiding a recession while bringing inflation down. Odds for a recession waned as belief the economy would have a soft landing increased.

Market expectations would be tempered though as inflation ticked back up and the Fed increased rates another quarter point (0.25%) at their July meeting. The Fed indicated additional interest rate increases were possible and rates would remain higher for longer. That ominous warning led to three straight months of negative returns for both the US stock market and US bond market. It was only the second time in history stocks and bonds had both lost money in three consecutive months. (Interestingly, the last time that happened was June through August 1966 and one year later stocks had returned 26.5% and bonds were up 7.1%.) By mid-October the 10-year Treasury had reached 5% for the first time since 2007.

Just as quickly as the market corrected on tempered expectations over the summer, it celebrated two consecutive meetings of the Fed pausing on interest rate increases (Sept and Nov) and inflation dipping back down.

A softening tone from the Fed was all that was needed for the market takeoff over the last two months of the year. The Bloomberg US Aggregate Bond Index posted its best monthly return since 1985 while the S&P 500 shot up more than 15%.

Outlook for 2024

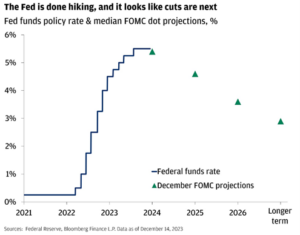

Despite the market rally, the ‘all clear’ has not been signaled yet. Markets are forward-looking and while the chances of a deep or long recession are easing, there are still risks to be navigated. Many economists are still calling for a recession. Inflation needs to be monitored – will the Fed err on the side of caution and remain too high for too long in attempt to bring inflation down to their preferred long-term average of 2%? Will interest rates subside quickly enough to stem potential refinancing issues within the commercial real estate market? The Fed has indicated they are likely to ease rates in the new year but any deviation from expectations could increase volatility.

Headlines will continue to focus on the negative as fear sells, and with the upcoming presidential election cycle just a few months away from hitting full steam, there will be increased noise and reasons to be fearful. Remember, if you are working with an advisor at Shakespeare, we have put in the time to develop a solid financial plan to weather the current environment. Give us a call with any questions and we wish you a very happy new year!