Shakespeare Blog: View from the Lake

Leveraging the Flexibility of 529 Plans

Written By: Brian Ellenbecker, CFP®, EA, CPWA®, CIMA®, CLTC®

529 plans have quickly become the vehicle of choice for families saving for education goals. Tax-free growth, a state tax deduction and ease-of-use are some of the main features that have led to their popularity. Fortunately, Congress has been very supportive of 529s as an education savings vehicle and continue to enhance the appeal of these accounts by making them even more flexible.

Key 529 Benefits

529 plans offer extensive tax advantages. Earnings grow tax free when used for qualified education expenses. Many states offer a deduction or credit for 529 plan contributions toward your state income tax liability. The plans are typically low cost and require little maintenance. Most offer “set it and forget it” investment plans that automatically adjust the asset allocation to a more conservative mix as the beneficiary gets closer to college.

Your annual gift exclusion of $16,000 can be used to make gift-tax-free contributions to the 529 plans. You can even front load the plans, using up to five years of exclusion gifts at a time. In other words, an individual can contribute $80,000 ($160,000 per couple) gift-tax-free.

In most cases, the account owner maintains control over the account. The beneficiary has no right to the funds (except in the case of a UTMA 529), so you don’t have to worry about them gaining access to the funds and using them in a way you didn’t intend.

Let’s examine some of the key planning opportunities that 529s offer in different situations.

Expecting Parents

New parents that want to get a jumpstart on saving for their new child’s education can open a 529 plan in one of their own names and start making contributions. Once the child is born and a Social Security number is issued, they can change the beneficiary from themself to their child. No tax consequences or penalties exist when a 529 plan beneficiary is changed to a member of the beneficiary’s family. Qualified family members include spouses, children, siblings, parents, in-laws, aunts and uncles, nieces and nephews, and first cousins.

The ability to change a 529 beneficiary to a different family member can add a lot of flexibility in how the account is used within a family.

Parents with Multiple Children

The ability to change beneficiaries can also help avoid the possibility of “overfunding” a 529.

For Example:

You have been diligently saving for college education for your three children. Your oldest has just completed their 4-year program. You had saved enough to help fund graduate school, if needed. Fortunately, your oldest found a great job in a career that won’t require additional schooling. However, there is still $20,000 left in their 529 plan. Fortunately, you can change the beneficiary on that account to one of your other children, who can use those funds tax-free on their upcoming education expenses.

Grandparents

Grandparents often want to contribute to the funding of their grandchildren’s educations. 529s are a great vehicle to assist with that goal.

Grandparents can typically fund 529s one of two ways: Either open a new 529 account where one of them is the owner or contribute to an existing 529. If you contribute to an existing 529 and want a state tax deduction, be sure the plan is sponsored by your home state. If it’s not, you will likely need to open one in your home state to get the state tax deduction.

In the past, distributions from grandparent-owned 529s were treated differently for FAFSA purposes. They used to be reported as untaxed income to the student, which could reduce the amount of aid available to them. Starting in the 2024-2025 award year, FAFSA will no longer require this type of income to be reported. Distributions from grandparent-owned 529 plans made in 2022 or later should no longer impact a student’s FAFSA application, assuming no additional delays.

Distributions from grandparent-owned 529s will likely still need to be included on the CSS profile, which is used by over 200 private institutions throughout the country.

To avoid these issues with reporting, grandparent-owned 529s could be a good funding source to pay for pre-college expenses, if that is a goal. You can use up to $10,000 per year per beneficiary for K-12 tuition expenses for public, private or parochial schools.

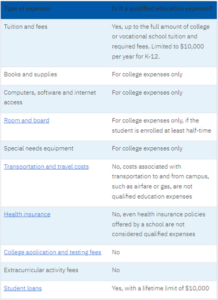

Qualified Expenses

529 funds can be withdrawn tax-free to pay for “qualified expenses”. The definition of qualified expenses has been expanding since 529s were introduced.

The table below from savingforcollege.com, highlights the most commonly asked about expenses and whether or not they are considered “qualified”.

Online classes are considered qualified expenses.

Unused Funds

You can withdraw funds from a 529 plan at any time, for any reason. However, withdrawals for non-qualified expenses will incur income taxes on the earnings along with an additional 10% penalty. States can impose additional taxes and penalties.

Money can be left in a 529 plan indefinitely. If you have funds left and no one else is expected to incur education expenses, you can leave the money in there. Perhaps there will be new family members (additional children or grandchildren, new spouses, etc.) that can use the money for education expenses or student loan payments down the road.

Education planning is an important part of your overall financial plan. Your Shakespeare advisor can help you achieve your goals of assisting loved ones with their education expenses and navigate the 529 rules.